3QFY2017 Result Update | Banking

February 13, 2017

ICICI Bank

ACCUMULATE

CMP

`282

Performance Highlights

Target Price

`315

Particulars (` cr)

Q3FY17

Q2FY17

% chg (qoq)

Q3FY16

% chg (yoy)

Investment Period

12 Months

NII

5,364

5,253

2.1

5,453

(1.6)

Pre-prov. profit

5,525

10,636

(48)

6,560

(15.8)

Stock Info

PAT

2,442

3,103

(21.3)

3,018

(19.1)

Source: Company, Angel Research

Sector

Banks

Market Cap (` cr)

1,63,997

ICICI Bank’s 3QFY17 results were in line with expectations. Though slippages

remained high, on an absolute basis it was lower sequentially and large part of

Beta

1.8

that came from the watch list. While overall loan book growth remained

52 Week High / Low

298/181

moderate, domestic business remained decent and fee income gained traction.

Avg. Daily Volume

14,83,994

Run down in overseas book impacted the overall loan book: Overall loan growth

Face Value (`)

2

remained muted up 5.2% YoY, flat QoQ. However, the domestic loan book grew

BSE Sensex

28,352

by 12% YoY. The international book reported decline of 16.1% due to the maturity

Nifty

8,805

of FCNR linked advances to the tune of $870Mn. The domestic loan growth

Reuters Code

ICBK.BO

continued to be driven by the retail loan portfolio which grew by 17.8% YoY.Retail

Bloomberg Code

ICICIBC@IN

loans contribution to the overall growth has been increasing off late and has gone

up to 48.9% for the quarter, compared to 43.8% in same period last year.

Deposit growth were healthy backed by flows in CASA, due to demonetization:

Shareholding Pattern (%)

Deposits grew by 14.2% yoy, after considering redemption of FCNR linked

Promoters

0.0

deposits to the tune of $1.75Bn, including which the deposit growth would

MF / Banks / Indian Fls

31.0

have been 17%+. There was fresh accretion of CASA to the tune of

`26,700cr, implying CASA growth of 15.9% YoY and 3.9% QoQ, thus the

FII / NRIs / OCBs

63.0

CASA ratio improved to 49.8% for Q3FY17 vs 45.7% in Q2FY17.

Indian Public / Others

6.0

Rise in GNPAs was on expected line; Gross slippages for the quarters were at

`7,037cr (6.1% slippages ratio) vs `8,029cr (7.1%). Of the total slippages ~94%

Abs.(%)

3m 1yr 3yr

came from the corporate accounts and 71% of the corporate slippages were from

the watch list itself. Of the total slippages ~94% came from the corporate

Sensex

5.7

23.3

40.4

accounts and 71% of the corporate slippages were from the watch list itself.

ICICIB

1.7

45.1

43.5

Accordingly, the amount of loans put under watch list came down to `27,536 cr vs

`32,490cr. With the current rate we believe large part of the troubled accounts of

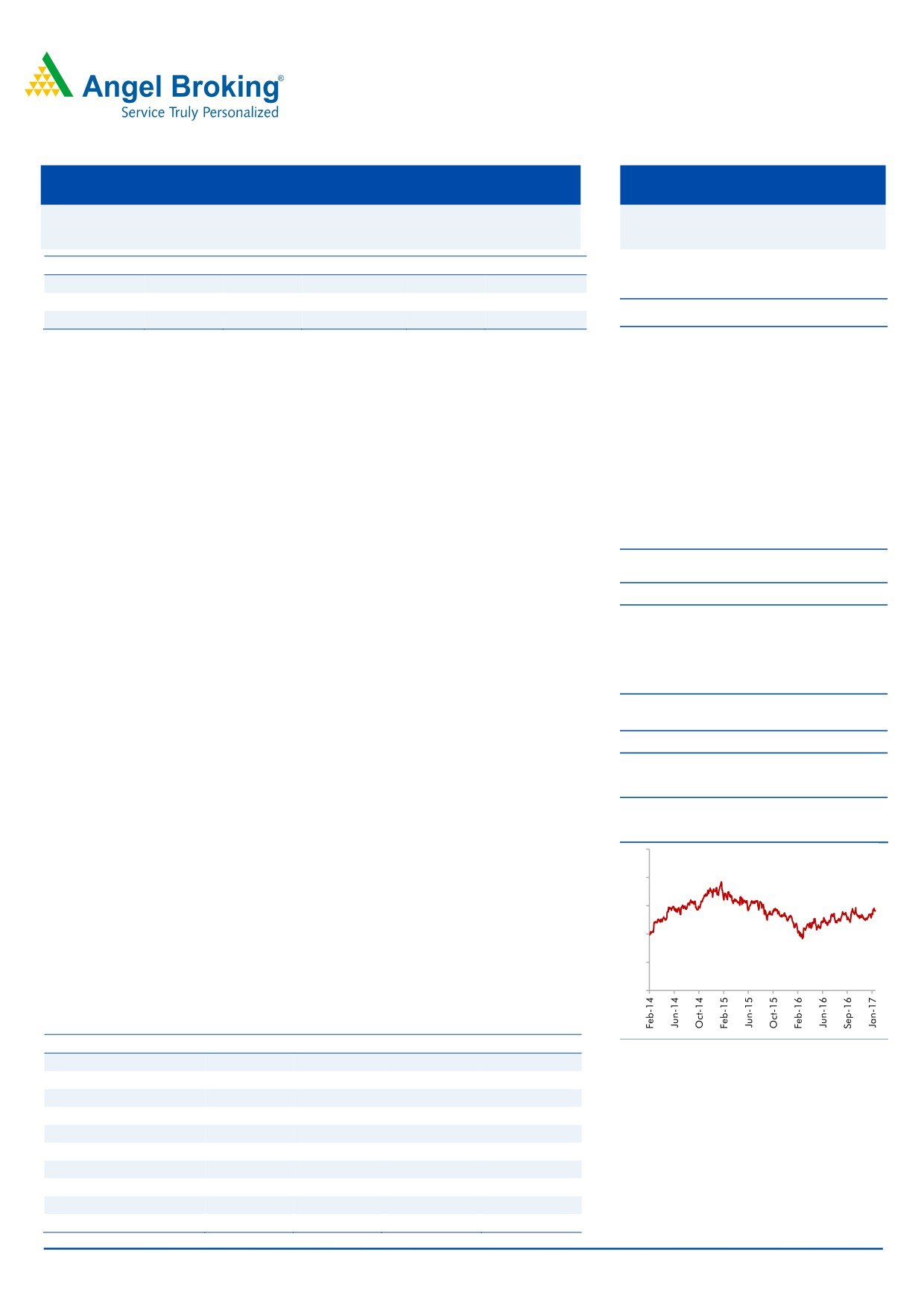

3-year price chart

the watch list should get over by FY18.

500

Outlook and valuation: While the near term outlook for ICICI Bank remains

400

challenging, the asset quality issues is gradually waning. The bank might choose

to grow slow as far as loan book is concerned which we believe is a right strategy.

300

At the current market price, the bank’s core banking business (after adjusting

200

`80/share towards the value of subsidiaries) is trading at 1.3x FY2018E ABV.

Though some pain in asset quality is likely to persist in the quarters to come, we

100

believe the current valuations remain decent for the bank and hence we have an

0

Accumulate rating on the stock, with a target price of `315.

Key financials (Standalone)

Y/E March (` cr)

FY2015

FY2016

FY2017E

FY2018E

Source: Company, Angel Research

NII

19,040

21,224

21,069

25,818

% chg

15.6

11.5

(0.7)

22.5

Net profit

11,176

9,726

10,160

11,748

% chg

13.9

(13.0)

4.5

15.6

NIM (%)

3.2

3.3

3.1

3.3

EPS (`)

19.3

16.7

17.4

20.2

P/E (x)

14.6

16.9

16.2

14.0

P/ABV (x)

2.2

2.2

2.0

1.9

Siddharth Purohit

RoA (%)

1.8

1.4

1.4

1.4

022 - 3935 7800 Ext: 6872

RoE (%)

14.5

11.4

10.5

10.8

Source: Company, Angel Research; Note: CMP as of February 13, 2017

Please refer to important disclosures at the end of this report

1

ICICI Bank | 3QFY2017 Result Update

Exhibit 1: 3QFY17 Income Statement ( Standalone)

Particulars (` cr)

Q1FY16

Q2FY16

Q3FY16

Q4FY16

Q1FY17

Q2FY17

Q3FY17

% YoY

% QoQ

Interest earned

12,813

13,099

13,346

13,482

13,330

13,639

13,618

2.0

(0.2)

- on Advances / Bills

9,375

9,665

9,863

10,041

9,837

9,905

9,870

0.1

(0.4)

- on investments

2,659

2,661

2,652

2,652

2,811

2,997

2,948

11.1

(1.6)

- on balance with RBI & others

32

31

36

59

50

38

126

246.6

231.0

- on others

747

741

795

730

632

699

675

(15.1)

(3.5)

Interest Expended

7,697

7,847

7,893

8,077

8,172

8,386

8,254

4.6

(1.6)

Net Interest Income

5,115

5,251

5,453

5,405

5,159

5,253

5,364

(1.6)

2.1

Other income

2,990

3,007

4,217

5,109

3,429

9,119

3,938

(6.6)

(56.8)

- Fee income

2,110

2,235

2,262

2,212

2,156

2,356

2,495

10.3

5.9

- Treasury income

673

550

513

707

505

5,682

-

(100.0)

(100.0)

- Others

207

222

1,442

2,190

768

729

893

(38.1)

22.5

Operating income

8,105

8,259

9,670

10,513

8,588

14,372

9,302

(3.8)

(35.3)

Operating expenses

3,067

3,100

3,110

3,406

3,373

3,736

3,778

21.5

1.1

- Employee expenses

1,267

1,213

1,140

1,382

1,291

1,556

1,406

23.3

(9.6)

- Other Opex

1,800

1,888

1,970

2,024

2,082

2,180

2,372

20.4

8.8

Pre-provision Profit

5,038

5,158

6,560

7,108

5,215

10,636

5,525

(15.8)

(48.1)

Provisions & Contingencies

955

942

2,844

6,926

2,515

7,082

2,713

(4.6)

(61.7)

PBT

4,082

4,216

3,716

181

2,700

3,554

2,812

(24.3)

(20.9)

Provision for Tax

1,106

1,186

698

(521)

446

451

369

(47.0)

(18.1)

PAT

2,976

3,030

3,018

(2,898)

2,254

3,103

2,442

(19.1)

(21.3)

Effective Tax Rate (%)

27

28

19

(287)

17

13

13

Source: Company, Angel Research

Exhibit 2: Loan Book Break Up

Particulars (` cr)

Q1FY16

Q2FY16

Q3FY16

Q4FY16

Q1FY17

Q2FY17

Q3FY17

% YoY

% QoQ

Domestic Corporate

1,14,725

1,16,353

1,25,222

1,19,698

1,27,637

1,25,829

1,29,921

3.8

3.3

Overseas branches

96,737

95,458

99,134

94,017

95,278

91,305

82,802

(16.5)

(9.3)

SME

17,189

17,617

20,001

18,716

17,977

19,533

21,044

5.2

7.7

Retail Total

1,71,088

1,80,265

1,90,442

2,02,833

2,08,534

2,17,588

2,23,703

17.5

2.8

-Home

93,927

99,326

1,04,553

1,09,530

1,13,234

1,18,150

1,22,142

16.8

3.4

-Vehicle loans

30,625

32,267

33,708

35,293

36,285

37,208

38,477

14.1

3.4

Rural

25,663

25,778

27,805

31,845

31,697

31,333

31,095

11.8

(0.8)

-Banking business

9,239

10,095

10,093

10,750

10,635

8,486

8,053

(20.2)

(5.1)

-Credit cards

4,106

4,507

5,142

5,476

5,839

6,092

7,158

39.2

17.5

-Personal loans

7,528

8,292

9,141

10,142

10,844

11,750

12,751

39.5

8.5

Others

4,569

4,027

-

-

Total advances

3,99,738

4,09,693

4,34,800

4,35,467

4,49,427

4,54,256

4,57,469

5.2

0.7

Source: Company, Angel Research

February 13, 2017

2

ICICI Bank | 3QFY2017 Result Update

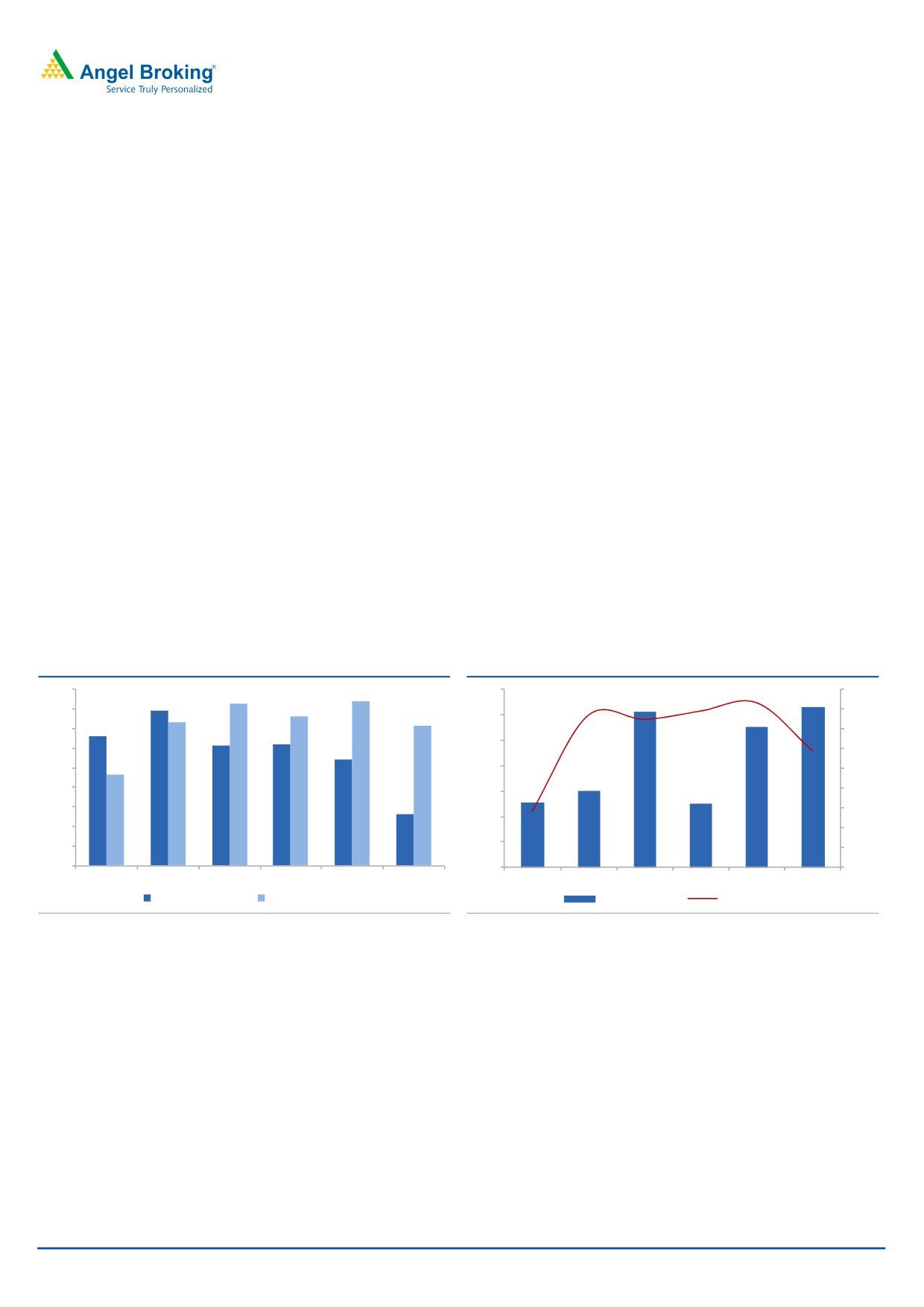

Domestic loan book grew at a healthy pace, run down in

overseas book impacted the overall loan book: Overall loan growth

remained muted up by only 5.2% YoY, and flat QoQ. However, the domestic loan

book grew by 12% YoY. The international book reported decline of 16.1% due to

the maturity of FCNR linked advances to the tune of $870Mn. The domestic loan

growth continued to be driven by the retail loan portfolio which grew by

17.8% YoY. However, the corporate loan book grew by a modest 4% as the

management remains focused and has been selective while lending to the large

corporates. SME portfolio also moderately grew by 6.6%.

Retail loans contribution to the overall growth has been increasing off late and has

gone up to 48.9% for the quarter, compared to 43.8% in same period last year.

Within the retail portfolio strong momentum was seen in the personal loans

segment up 39.9% and credit card business up 39.7%. With lower incremental

credit demand from corporates the growth will continue to be driven by the retail

segment for ICICI Bank in the quarters to come.

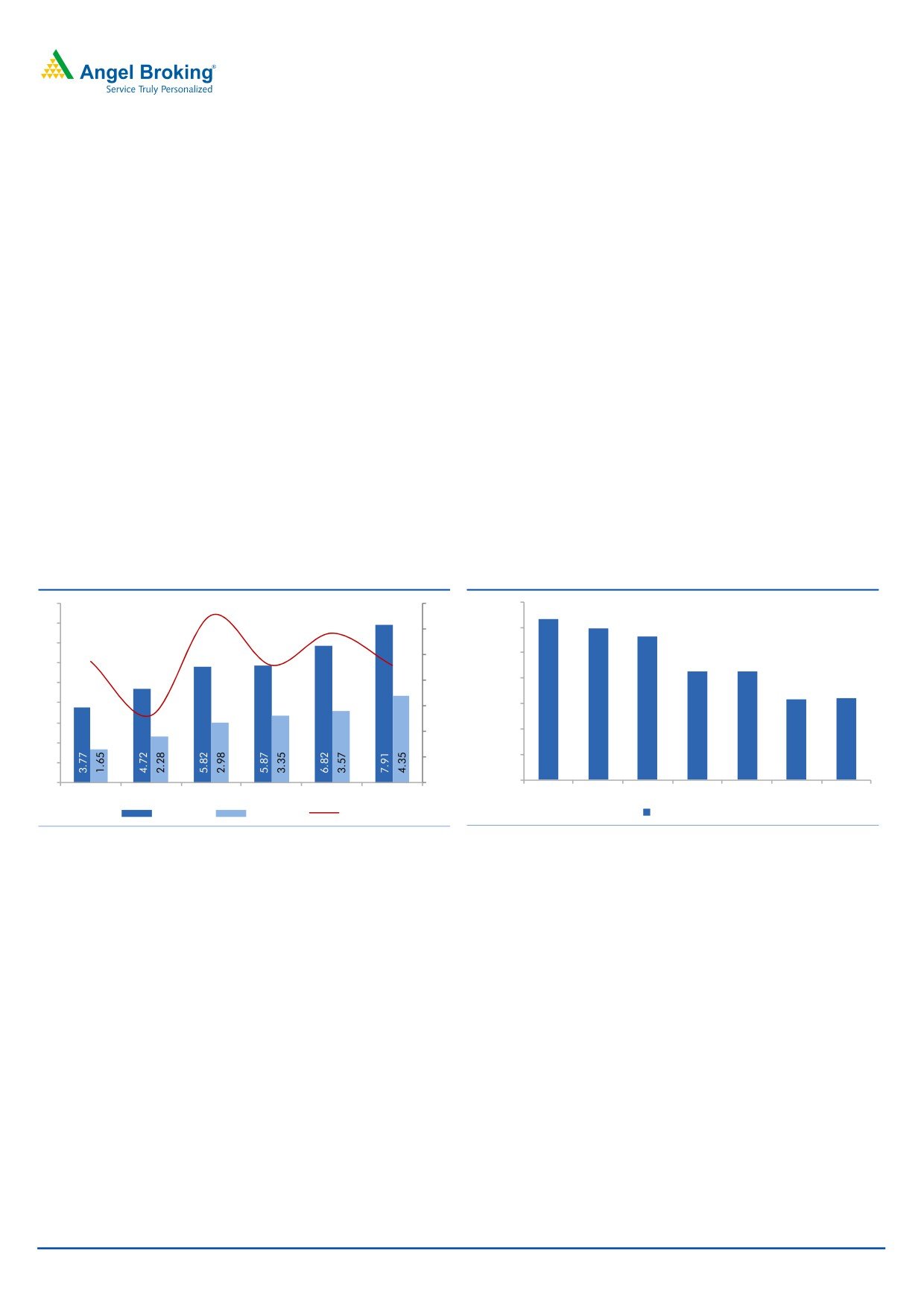

Deposit growth were healthy backed by flows in CASA, due to demonetization:

Deposits grew by 14.2% yoy, after considering redemption of FCNR linked

deposits to the tune of $1.75Bn, including which the deposit growth would have

been 17%+. There was fresh accretion of CASA to the tune of `26,700cr, implying

CASA growth of 15.9% YoY and 3.9% QoQ, thus the CASA ratio improved to

49.8% for Q3FY17 vs 45.7% in Q2FY17.

Exhibit 3: Loan Growth

Exhibit 4: CASA Growth trend

18.0

16.6

16.8

46.0

17.9

18.3

19.0

15.8

17.7

15.3

17.5

16.0

14.6

18.0

14.2

45.8

13.3

14.0

17.0

12.3

12.4

15.9

45.6

12.0

10.9

16.0

9.2

45.4

10.0

15.0

8.0

14.0

45.2

12.9

5.2

6.0

13.0

45.0

4.0

12.0

44.8

2.0

11.0

45.1

45.2

45.8

45.1

45.7

45.9

0.0

44.6

10.0

Q2FY16

Q3FY16

Q4FY16

Q1FY17

Q2FY17

Q3FY17

Q2FY16

Q3FY16

Q4FY16

Q1FY17

Q2FY17

Q3FY17

Loan Growth YoY (%) Deposit Growth YoY (%)

CASA Ratio (%)

YoY Growth (%)

Source: Company, Angel Research

Source: Company, Angel Research

February 13, 2017

3

ICICI Bank | 3QFY2017 Result Update

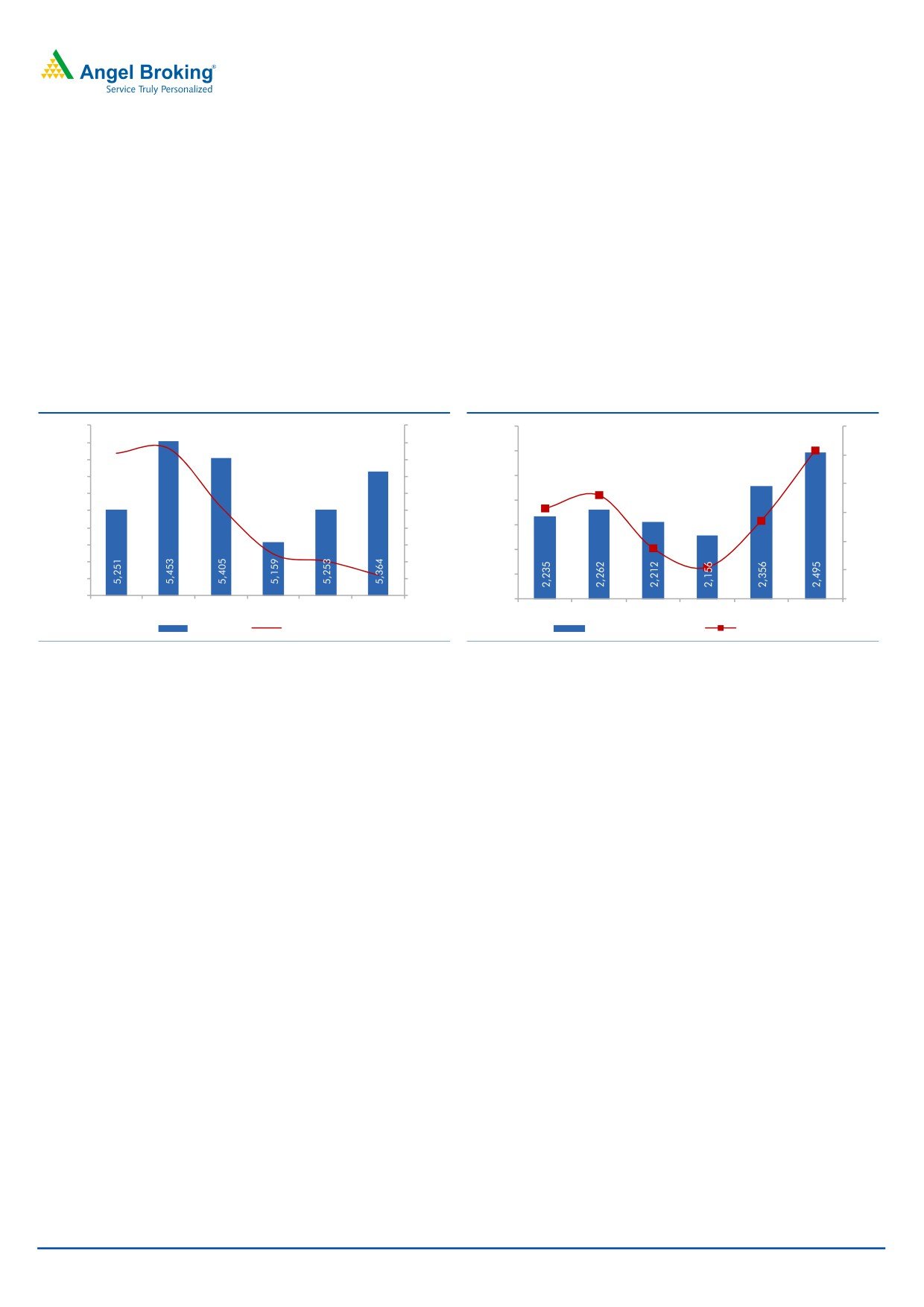

NII remained under pressure, while fee income supported bottom-line: NII

continued to be under pressure and declined by 1.6% yoy, which can be attributed

to the subdued loan growth and interest reversal due to slippages. After remaining

subdued in the previous few quarters, fee income picked up and grew by 10% and

traction in the fee income is expected to remain healthy in the quarters to come.

Retail fees grew by 18% YoY and retail fees contributed to 71% of the total fees.

Further credit cost remained under control for the quarter and this helped in PAT at

`2442cr, which though declined by

19% YoY, still was better than our

expectations. As slippages are expected to remain high in the quarters to come,

the NII will also be under pressure in the coming quarters.

Exhibit 5: NII Growth remained subdued

Exhibit 6: Fee Income growth picked up

5,500

16.0

2,600

12.0

5,450

14.0

13.3

2,500

12.8

10.3

10.0

5,400

12.0

5,350

10.0

2,400

7.2

8.0

5,300

8.0

2,300

5,250

6.4

6.0

6.3

6.0

2,200

5.4

5,200

4.0

5,150

2.0

4.0

2,100

3.5

0.8

5,100

0.0

0.0

2.2

2.0

-1.

6

2,000

5,050

-2.0

5,000

-4.0

1,900

0.0

Q2FY16

Q3FY16

Q4FY16

Q1FY17

Q2FY17

Q3FY17

Q2FY16

Q3FY16

Q4FY16

Q1FY17

Q2FY17

Q3FY17

NII (` Cr)

% YoY Growth

Fee Income (` Cr)

YoY Growth (%)

Source: Company, Angel Research

Source: Company, Angel Research

February 13, 2017

4

ICICI Bank | 3QFY2017 Result Update

Rise in GNPAs was on expected line: The GNPAs went up by 17% QoQ to

`37,716cr and GNPAs % went up by 110 bps to 7.91%. However, the rise in

GNPAs was on the expected line. As indicated by the management earlier large

part of the slippages came from the list of accounts put under watch. Gross

slippages for the quarters were at `7,037cr (6.1% slippages ratio) vs `8,029cr

(7.1%). Of the total slippages ~94% came from the corporate accounts and 71%

of the corporate slippages were from the watch list itself. Accordingly, the amount

of loans put under watch list came down to `27,536cr vs `32,490cr.

With the current rate we believe large part of the troubled accounts of the watch list

should get over by FY18. While absolute slippages could remain high, the good

part is that only 24% of the total slippages were from the non-watch list corporate

accounts while the large part continued to come from the watch list, which

indicates that the trouble of asset quality remains restricted to the watch list.

Couple of mid-sized accounts got restructured during the quarter and outstanding

restructured loan book inched up marginally to `6,407 cr. Outstanding SDR loans

stood at `3,400 cr , of which `2,800 cr from NPAs, while outstanding 5:25 stood

at `3,300 cr, of which `2400 cr were from loans under watch list.

Exhibit 7: GNNPAs & NNPAs went up

Exhibit 8: Restructured loan book remained stable

9

62

14,000

12,604

61.0

11,868

8

11,294

60

12,000

59.6

7

57.4

58

10,000

8,573

8,573

6

57.1

57.1

56

8,000

5

6,336

6,407

4

54

6,000

53.2

3

52

4,000

2

50

2,000

1

0

48

-

Q2FY16

Q3FY16

Q4FY16

Q1FY17

Q2FY17

Q3FY17

Q1FY16

Q2FY16

Q3FY16

Q4FY16

Q1FY17

Q2FY17

Q3FY17

GNPAs %

NNPAs %

PCR %

O/S Restrctured Book

Source: Company, Angel Research

Source: Company, Angel Research

February 13, 2017

5

ICICI Bank | 3QFY2017 Result Update

Outlook and Valuation

While the near term outlook for ICICI Bank remains challenging, the asset quality

issues is gradually waning. The bank might choose to grow slow as far as loan

book is concerned which we believe is a right strategy. At the current market price,

the bank’s core banking business (after adjusting `80/share towards the value of

subsidiaries) is trading at 1.3x FY2018E ABV. Though some pain in asset quality is

likely to persist in the quarters to come, we believe the current valuations remain

decent for the bank and hence we have an Accumulate rating on the stock, with a

target price of `315.

Exhibit 9: SOTP valuation summary

Particulars

Target multiple Value/share (`)

ICICI Bank

1.6x FY2018E ABV

229

Life Insurance

Based on Market Price

40

General Insurance

Based On Deal Value

21

Others (Home Fin, AMC, VC, Securities

25

PD and Overseas subsidiaries)

SOTP value

315

Source: Angel Research

Company Background

ICICI Bank is India's largest private sector bank, with ~ 5% market share in credit.

The bank has a pan-India extensive network of 4,504 branches and around

14,146 ATMs. The bank has a large overseas presence (overseas loans comprise

~18.1% of total loans). The bank also has market-leading subsidiaries in life

insurance, general insurance and asset management segments.

February 13, 2017

6

ICICI Bank | 3QFY2017 Result Update

Income statement (Standalone)

Y/E March (` cr)

FY13

FY14

FY15

FY16

FY17E

FY18E

Net Interest Income

13,866

16,476

19,040

21,224

21,069

25,818

- YoY Growth (%)

29.2

18.8

15.6

11.5

(0.7)

22.5

Other Income

8,346

10,428

12,176

15,323

20,737

16,175

- YoY Growth (%)

11.2

24.9

16.8

25.8

35.3

-22.0

Operating Income

22,212

26,903

31,216

36,547

41,805

41,993

- YoY Growth (%)

21.8

21.1

16.0

17.1

14.4

0.4

Operating Expenses

9,013

10,309

11,496

12,684

14,575

16,536

- YoY Growth (%)

14.8

14.4

11.5

10.3

14.9

13.5

Pre - Provision Profit

13,199

16,595

19,720

23,863

27,230

25,457

- YoY Growth (%)

27.1

25.7

18.8

21.0

14.1

(6.5)

Prov. & Cont.

1,803

2,626

3,900

11,668

15,213

8,053

- YoY Growth (%)

13.9

45.7

48.5

199.2

30.4

(47.1)

Profit Before Tax

11,397

13,968

15,820

12,196

12,016

17,404

- YoY Growth (%)

29.5

22.6

13.3

(22.9)

(1.5)

44.8

Prov. for Taxation

3,071

4,158

4,644

2,469

1,857

5,656

- as a % of PBT

26.9

29.8

29.4

20.2

15.5

32.5

PAT

8,325

9,810

11,176

9,726

10,160

11,748

- YoY Growth (%)

28.8

17.8

13.9

(13.0)

4.5

15.6

Balance sheet (Standalone)

Y/E March (` cr)

FY13

FY14

FY15

FY16

FY17E

FY18E

Share Capital

1,154

1,155

1,160

1,163

1,165

1,165

Reserve & Surplus

65,552

72,052

79,262

88,566

1,03,455

1,11,678

Deposits

2,92,614

3,31,914

3,61,563

4,21,426

4,74,590

5,47,221

- Growth (%)

14.5

13.4

8.9

16.6

12.6

15.3

Borrowings

1,45,341

1,54,759

1,72,417

1,74,807

1,66,106

2,07,944

- Growth (%)

3.7

6.5

11.4

1.4

-5.0

25.2

Other Liab. & Prov.

32,134

34,756

31,720

34,726

37,967

49,250

Total Liabilities

5,36,795

5,94,642

6,46,129

7,20,688

7,83,283

9,17,258

Cash in Hand and with

19,053

21,822

25,653

27,106

28,475

32,833

RBI

Bal.with banks & money

22,365

19,708

16,652

32,763

20,170

23,257

at call

Investments

1,71,394

1,77,022

1,86,580

1,60,412

1,89,005

2,37,877

Advances

2,90,249

3,38,703

3,87,522

4,35,264

4,71,194

5,45,930

- Growth (%)

14.4

16.7

14.4

12.3

8.3

15.9

Fixed Assets

4,647

4,678

4,726

7,577

6,882

7,935

Other Assets

29,087

32,709

24,997

57,567

67,557

69,426

Total Assets

5,36,795

5,94,642

6,46,129

7,20,688

7,83,283

9,17,258

February 13, 2017

7

ICICI Bank | 3QFY2017 Result Update

Ratio analysis (Standalone)

Y/E March

FY13

FY14

FY15

FY16

FY17E

FY18E

Profitability ratios (%)

NIMs

2.9

3.1

3.2

3.3

3.1

3.3

Cost to Income Ratio

40.6

38.3

36.8

34.7

34.9

39.4

RoA

1.6

1.7

1.8

1.4

1.4

1.4

RoE

13.1

14.0

14.5

11.4

10.5

10.8

B/S ratios (%)

CASA Ratio

41.9

42.9

45.5

45.8

45.9

46.1

Credit/Deposit Ratio

99.2

102.0

107.2

103.3

99.3

99.8

CAR

18.7

17.7

17.0

16.6

16.8

15.8

- Tier I

5.9

4.9

4.2

3.5

3.4

3.1

Asset Quality (%)

Gross NPAs

3.2

3.0

3.8

5.8

7.4

6.7

Net NPAs

0.6

1.0

1.6

3.0

4.6

4.5

Slippages

1.4

1.7

2.4

4.4

3.7

2.6

Loan Loss Prov. /Avg. Assets

0.6

0.8

1.0

2.7

3.2

1.5

Provision Coverage

76.8

70.4

59.1

50.3

52.0

52.5

Per Share Data (`)

EPS

14.4

17.0

19.3

16.7

17.4

20.2

ABVPS

111.8

121.1

127.9

129.5

142.2

151.7

DPS

4.0

4.4

4.8

5.0

5.0

6.0

Valuation Ratios

PER (x)

19.5

16.6

14.6

16.9

16.2

14.0

P/ABVPS (x)

2.5

2.3

2.2

2.2

2.0

1.9

Dividend Yield

1.4

1.6

1.7

1.8

1.8

2.1

DuPont Analysis

NII

2.7

2.9

3.1

3.1

2.8

3.0

(-) Prov. Exp.

1.6

1.8

2.0

2.2

2.8

1.9

Adj NII

4.3

4.8

5.0

5.3

5.6

4.9

Other Inc.

1.8

1.8

1.9

1.9

1.9

1.9

Op. Inc.

2.6

2.9

3.2

3.5

3.6

3.0

Opex

0.4

0.5

0.6

1.7

2.0

0.9

PBT

2.2

2.5

2.6

1.8

1.6

2.0

Taxes

0.6

0.7

0.7

0.4

0.2

0.7

ROA

1.6

1.7

1.8

1.4

1.4

1.4

Leverage

8.1

8.1

8.1

8.0

7.7

7.8

RoE

13.1

14.0

14.5

11.4

10.5

10.8

February 13, 2017

8

ICICI Bank | 3QFY2017 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public

offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Disclosure of Interest Statement

ICICI Bank

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives

No

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

February 13, 2017

9